Payday loan alternatives are lower-cost ways to cover a short-term cash gap without the triple-digit APRs and rollover traps of payday lending. With the average payday APR near 391%, almost any alternative saves you money. This guide walks through seven safer options, roughly in order of cost, so you can find the cheapest one you qualify for.

Quick answer: The safest payday loan alternatives include credit-union Payday Alternative Loans (APR capped at 28%), small personal installment loans, paycheck advance apps, a 0% credit-card grace period, borrowing from family, employer advances, and local assistance programs. Each costs far less than a payday loan’s ~391% APR.

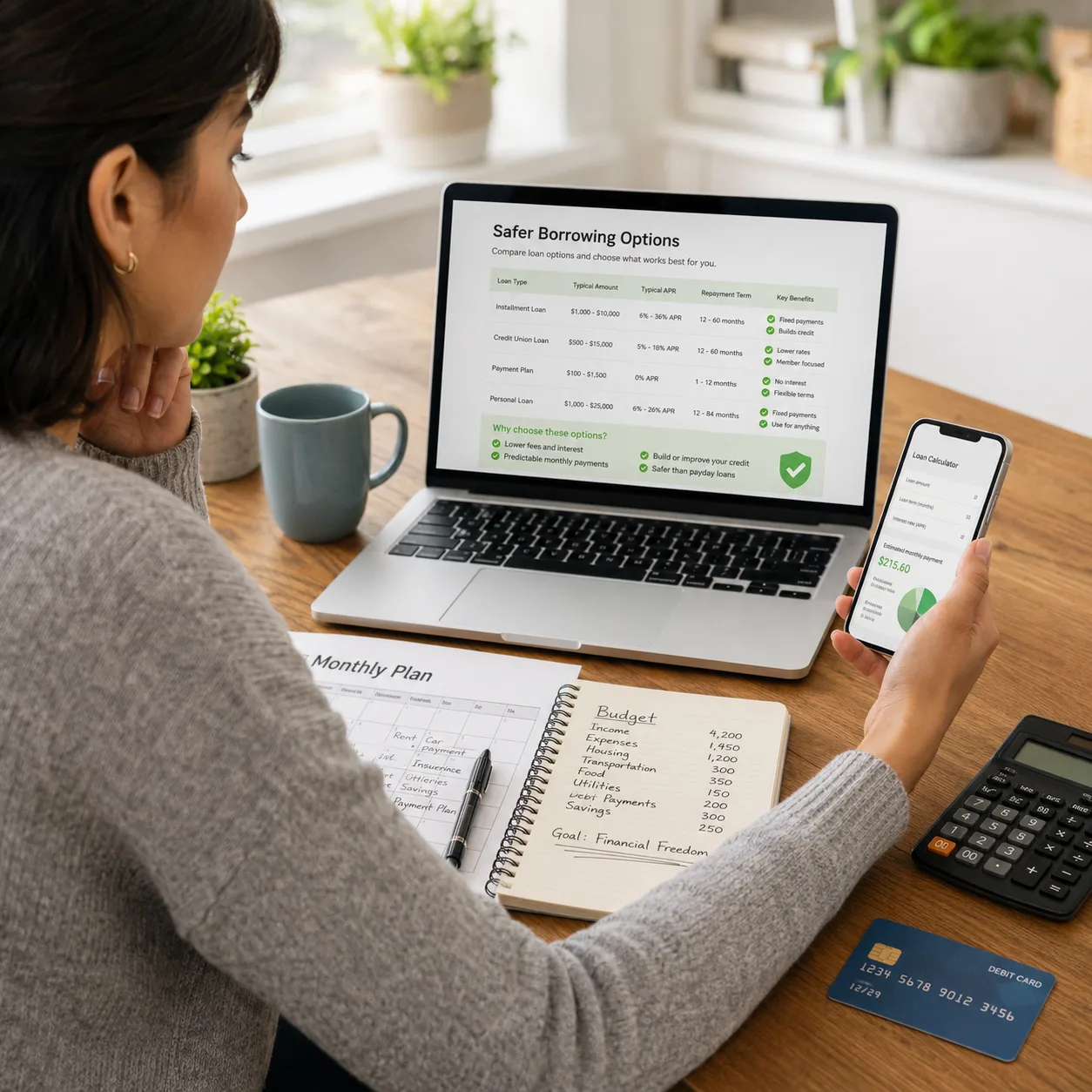

Seven safer options

- Payday Alternative Loans (PALs). Offered by federal credit unions, with APR capped at 28% and small, affordable amounts.

- Small personal installment loans. Online and credit-union loans with APRs typically in the 8%–36% range, repaid over months.

- Paycheck advance apps. Earned-wage access tools that advance part of your pay, often for a small fee or tip.

- Credit-card cash flow. Using an existing card within its grace period, or a 0% intro offer, beats payday APRs even with card interest.

- Family or friends. An interest-free loan, with clear written terms to protect the relationship.

- Employer advance. Many employers will advance earned wages with no fee.

- Local assistance. Community programs, nonprofits, and utility hardship plans can cover essentials directly.

How the costs compare

| Option | Typical cost | Best for |

|---|---|---|

| Payday loan | ~391% APR | Almost never the best choice |

| PAL (credit union) | Up to 28% APR | Small emergencies, members |

| Personal installment loan | 8%–36% APR | Larger amounts over time |

| Paycheck advance app | Small fee or tip | Bridging to next payday |

| Employer advance | Often free | Quick, no-interest gap fill |

Before you borrow at all

Sometimes the cheapest option is not a loan. Ask creditors for a short payment extension, tap an emergency fund, sell unused items, or contact a nonprofit credit counselor. If you do borrow, choose the lowest-APR option you qualify for and confirm you can repay on schedule.

FAQ

What is the cheapest alternative to a payday loan?

Usually an employer advance or an interest-free loan from family, followed by a credit-union Payday Alternative Loan capped at 28% APR. All cost a tiny fraction of a payday loan’s average ~391% APR.

Can I get a payday loan alternative with bad credit?

Yes. PALs, paycheck advance apps, and many small installment loans are designed for borrowers with limited or poor credit, and they remain far cheaper than payday loans.

Are paycheck advance apps safe?

Reputable earned-wage access apps are generally safe and inexpensive, but watch for high optional “tips” or fast-funding fees that can add up. Read the terms and treat repeated use as a sign to address the underlying cash-flow gap.

Educational content, not financial advice. If you are facing ongoing cash shortfalls, a nonprofit credit counselor can help.